Remote Homes (No Fire Hydrants): Insurance Challenges in Canada

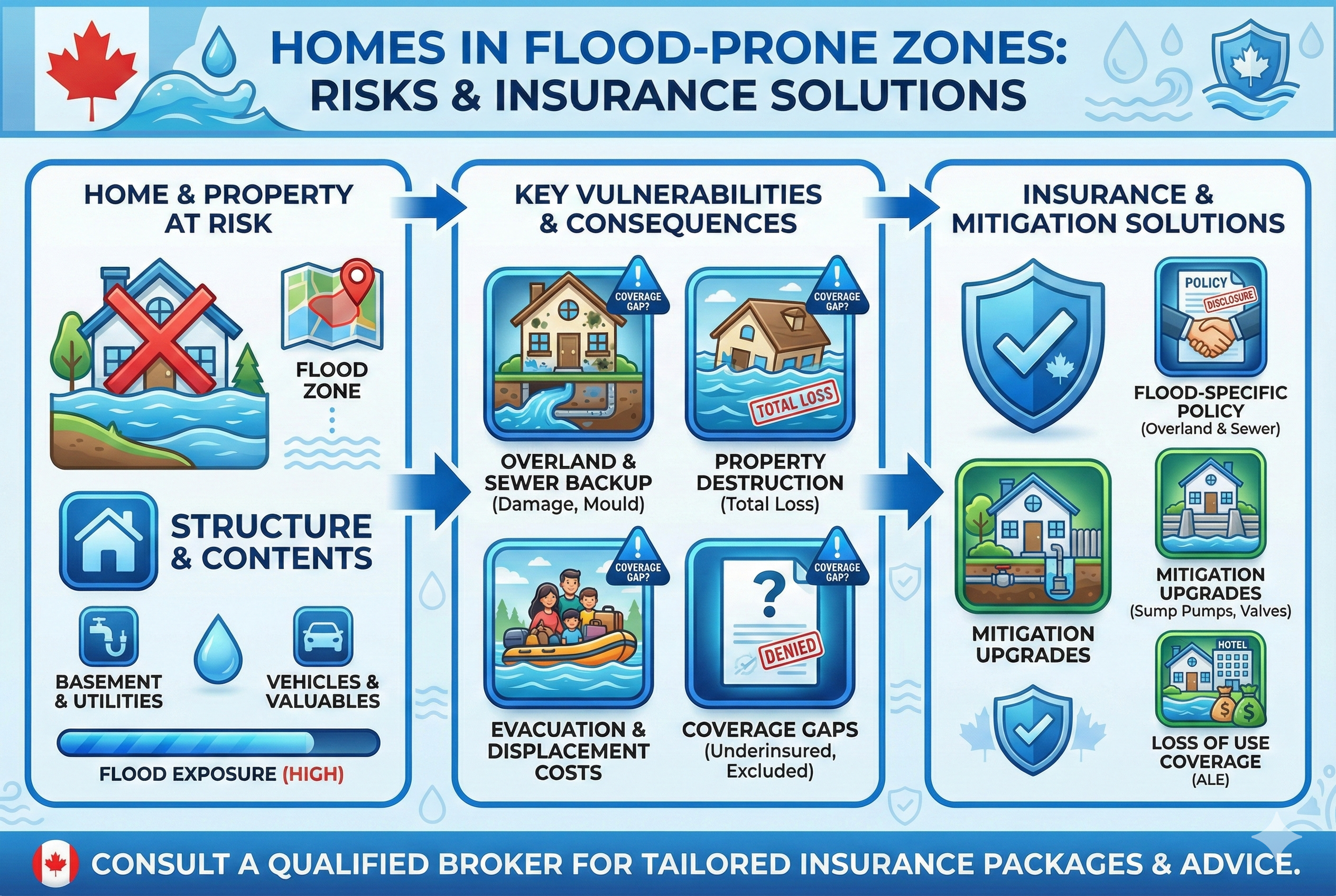

Homes in Flood-Prone Zones: What Canadian Homeowners Should Know

February 9, 2026

Rented Dwellings: Insurance Essentials for Canadian Property Owners

February 11, 2026

Remote and rural homes offer privacy, space, and breathtaking surroundings—but when there are no nearby fire hydrants, insurance risk increases significantly. In Canada, limited fire protection is one of the biggest factors affecting home insurance availability and cost.

Why Fire Protection Matters

Insurers assess:

- Distance to the nearest fire station

- Availability of water sources (hydrants, lakes, cisterns)

- Local fire department response capabilities

Homes far from hydrants or municipal services may face:

- Higher premiums

- Increased fire deductibles

- Coverage restrictions or limited insurer options

Key Insurance Considerations

- Fire Coverage Limits – Ensure limits reflect full rebuild costs

- Guaranteed Replacement Cost – Rising construction costs matter more in remote areas

- Debris Removal & Cleanup – Often higher due to access challenges

- Additional Living Expenses – Repairs can take longer in rural locations

How to Reduce Risk (and Premiums)

- Install monitored smoke & fire alarms

- Add sprinklers or water storage tanks

- Maintain clear access roads for fire crews

- Document fire-mitigation upgrades for your insurer

Final Thought

Remote living doesn’t mean uninsurable—but it does require smart planning and tailored coverage. The right prevention steps and an experienced Canadian broker can help protect your home and peace of mind. 🇨🇦

Brokers can contact Total Risk Managers to discuss a risk.

This article is general information for insurance brokers. It is not advice, and it is not a quote or an offer of coverage. Policy wording decides what is covered. Coverage is arranged through a licensed insurance broker.

{kind=link}