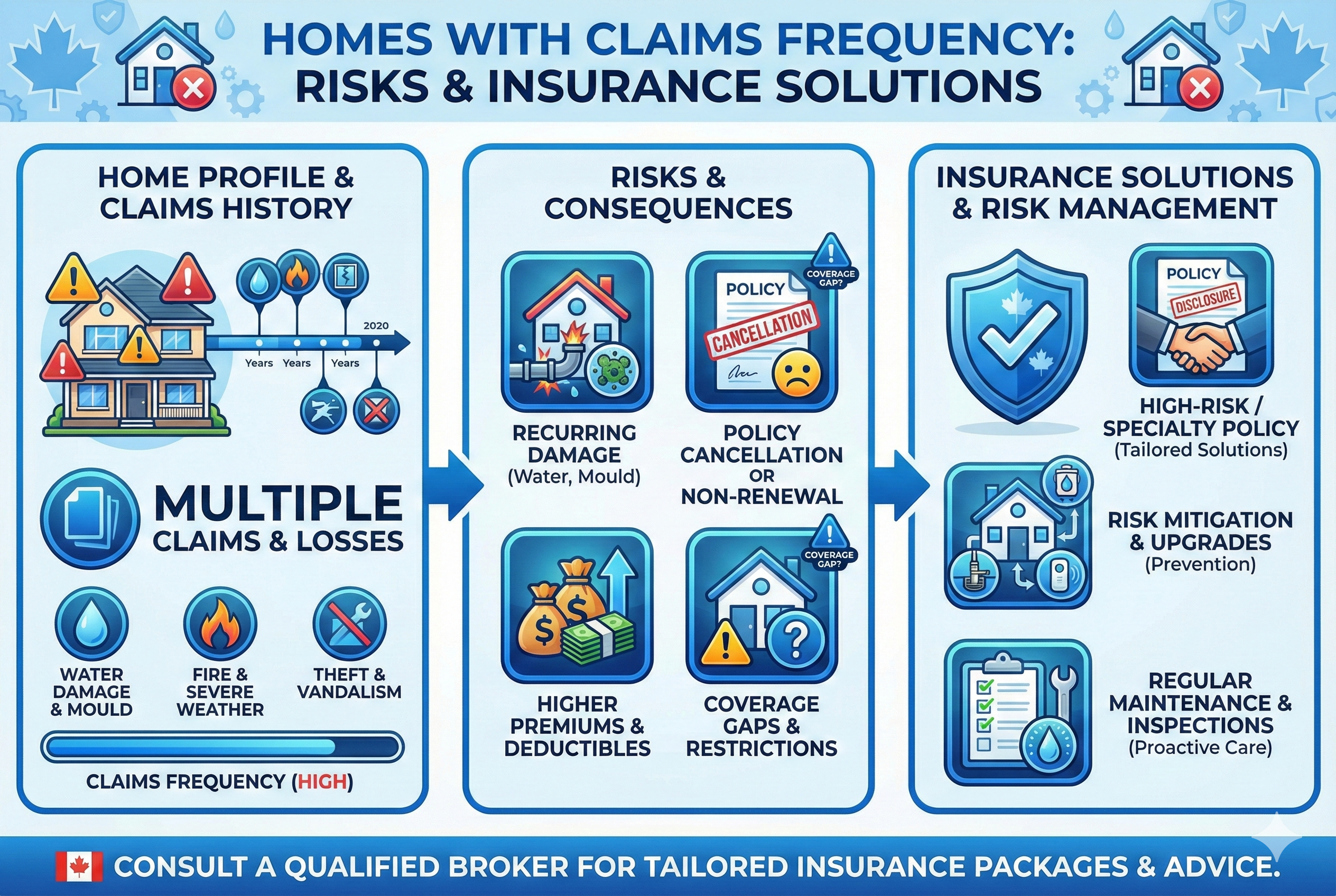

Homes With Claims Frequency: What Canadian Homeowners Need to Know

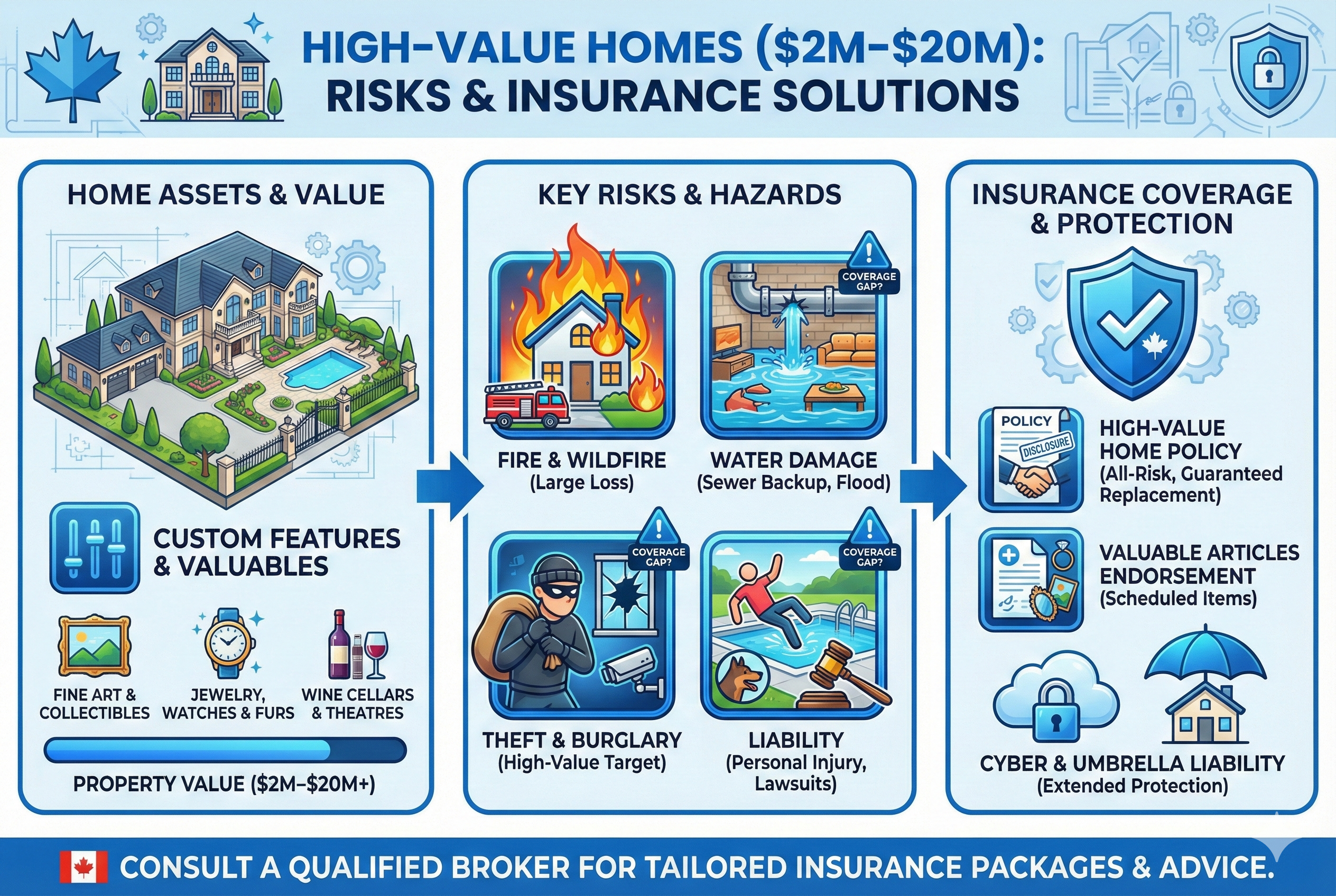

High-Value Homes ($2M–$20M): Insurance Considerations in Canada

February 5, 2026

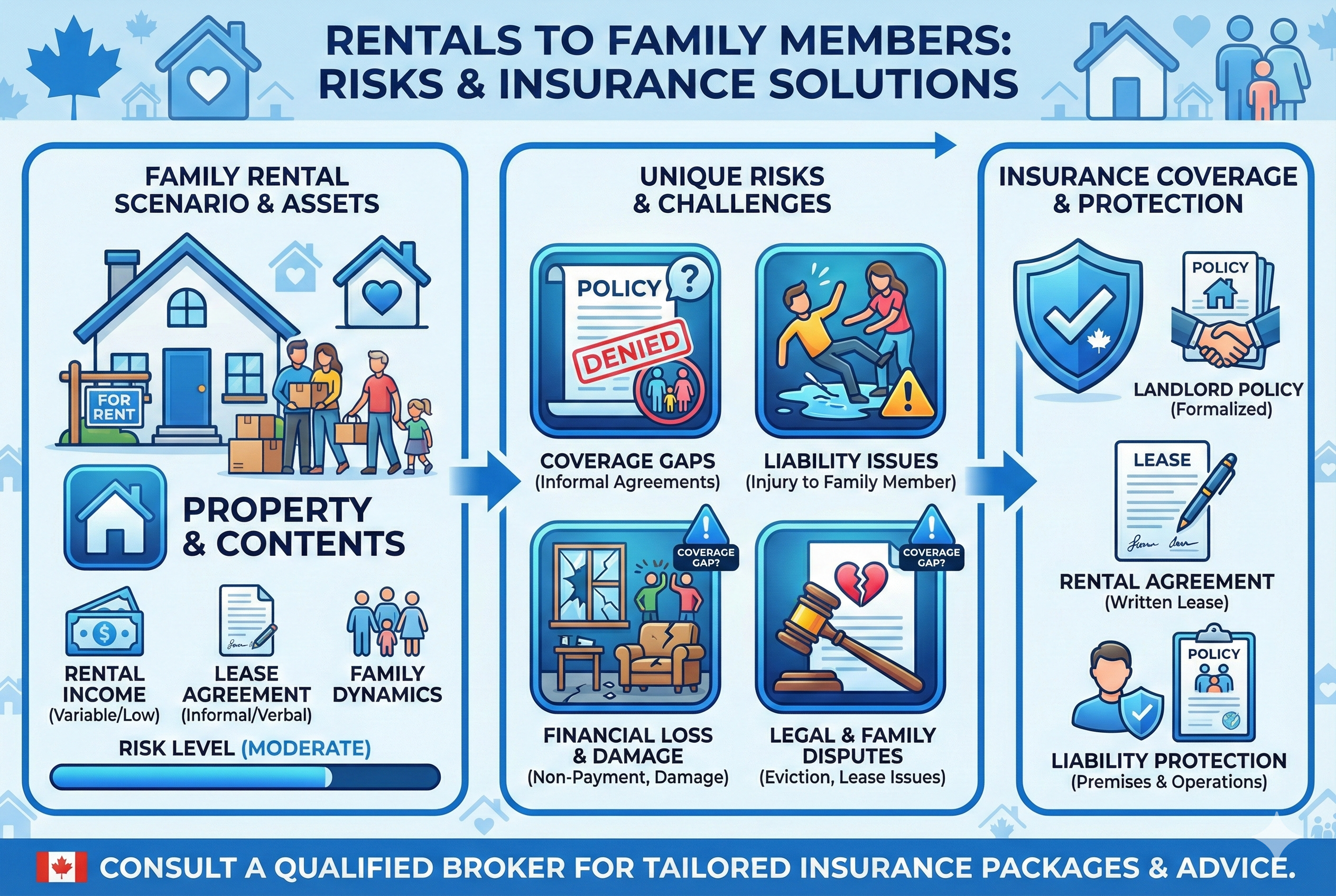

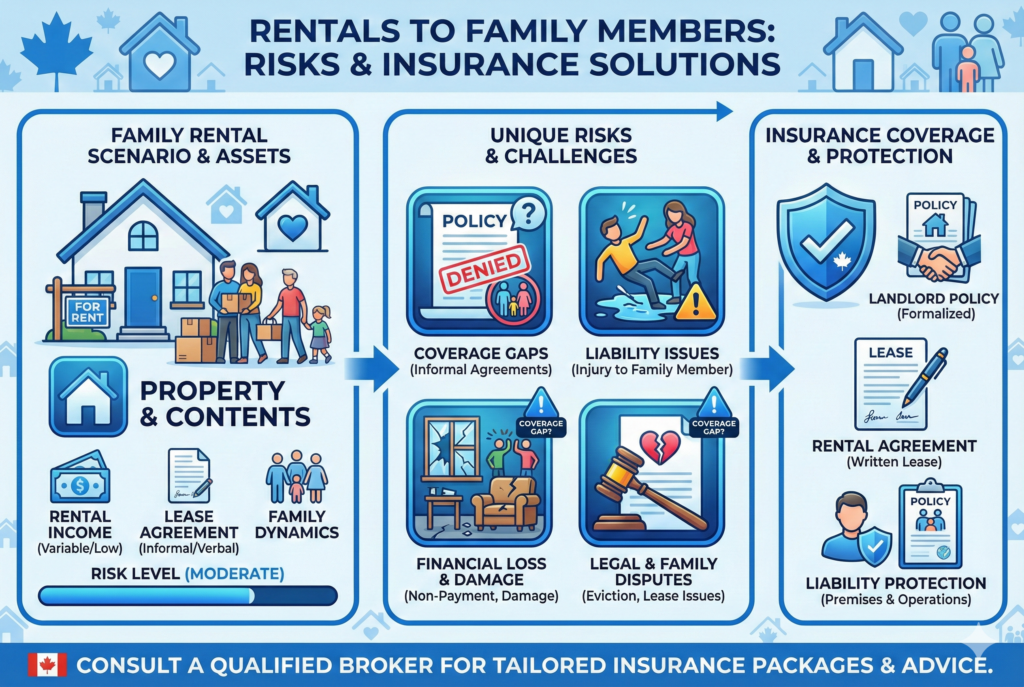

Homes in Wildfire Zones: Insurance Realities for Canadian Homeowners

February 7, 2026

If your home has a history of frequent insurance claims, getting (and keeping) coverage in Canada can become increasingly difficult. Insurers closely track claims frequency—not just severity—when assessing risk. Even smaller, repeated claims can raise red flags. 🚩

Why Claims Frequency Matters

Multiple claims within a short period—especially for water damage, fire, theft, or liability—signal ongoing risk. Insurers may respond by:

- Increasing premiums 💸

- Applying higher deductibles 📈

- Restricting coverage (e.g., water exclusions) 🚫

- Declining renewal altogether ❌

Common High-Frequency Claim Triggers

- Repeated water losses from aging plumbing 💧

- Basement flooding or sewer backups 🌊

- Theft or vandalism in high-traffic areas 🕵️♂️

- Slip-and-fall liability incidents ⚖️

How to Improve Insurability

- Invest in risk prevention: Upgrade plumbing, install backwater valves & leak detectors 🛠️

- Avoid small claims: Handle minor repairs out of pocket when possible 🧾

- Document upgrades: Show insurers you’ve reduced risk 📸

- Work with a broker: Access insurers that specialize in higher-risk homes 🤝

Final Thought

A claims history doesn’t end your insurability—but ignoring the root causes can. Proactive risk management and expert guidance can help stabilize coverage and costs. 🇨🇦🛡️

#HomeInsuranceCanada #ClaimsHistory #PropertyInsurance #RiskManagement #InsuranceTips #CanadianHomeowners #WaterDamageClaims #HighRiskHomes #InsuranceSolutions

{kind=link}