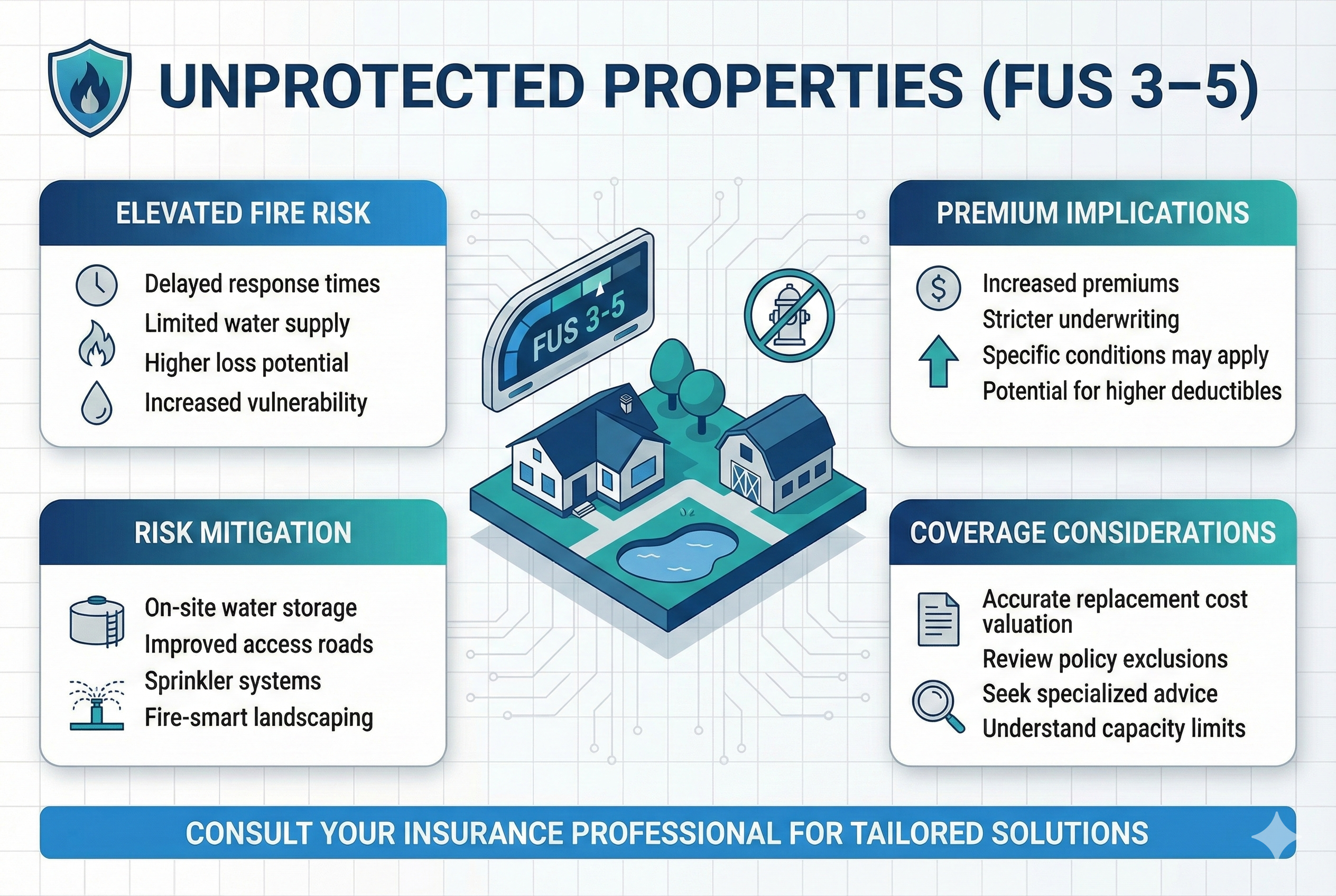

Rural Properties with Limited Fire Response: What You Need to Know

Unprotected Properties (FUS 3–5): Insurance Considerations for Property Owners

December 19, 2025

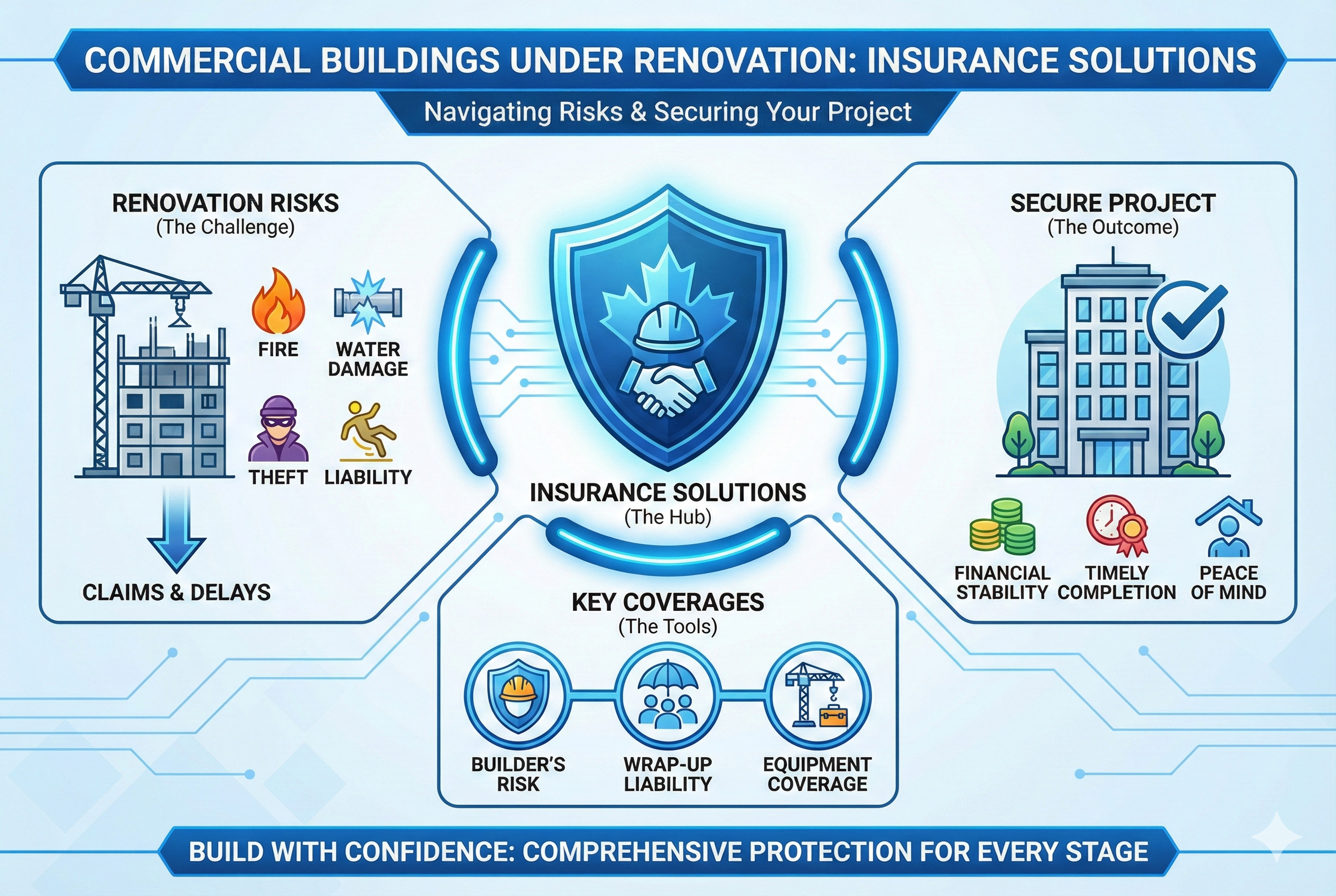

Commercial Buildings Under Renovation: What Canadian Business Owners Need to Know

December 22, 2025

Living in the countryside offers peace, space, and natural beauty, but it also comes with its own set of challenges—especially when it comes to fire safety. In many rural areas across Canada, fire response times can be slower, and fire services may be limited. 🔥🚒

When it comes to insurance for rural properties, fire risk is one of the top concerns. Limited fire response can significantly increase the chances of severe damage from wildfires or house fires, leading insurers to charge higher premiums or even refuse coverage.

Key Factors:

- Distance from Fire Services: Insurance companies assess the distance between your property and the nearest fire station. The further away, the higher your risk—and the higher your premium.

- Fire Prevention Measures: Adding firebreaks, sprinkler systems, and clearing brush can reduce the risk and may help lower insurance costs.

- Local Risks: Some regions are more prone to wildfires (e.g., British Columbia, Alberta), making fire protection even more crucial.

- Policy Exclusions: Always review your insurance policy for any fire-related exclusions. Ensure it covers all potential risks.

🌿 Tip: Consult with a local insurance broker to tailor your coverage to your specific needs, ensuring you’re properly protected.

RuralPropertyInsurance #FireRiskCanada #LimitedFireResponse #WildfireProtection #RuralLivingCanada #HomeInsuranceTips #FireSafetyPreparedness #CanadianHomeowners #RiskManagementCanada #PropertyProtection

{kind=link}